By Saqib Iqbal Ahmed and Suzanne McGee

NEW YORK (Reuters) - Corners of financial markets that could feel the impact of a Donald Trump victory are stirring again, as the U.S. presidential race tightens with less than three weeks until Election Day.

Assets ranging from small-cap stocks to bitcoin have climbed in recent weeks while the Mexican peso and Treasuries have slipped, as polls show a tight race between Republican candidate Trump and his Democratic opponent, Vice President Kamala Harris.

The moves echo the so-called Trump trades from earlier this year when he pulled ahead of President Joe Biden, only to fade after Biden withdrew.

Harris led Trump by a marginal 45% to 42% in a Reuters/Ipsos poll released on Tuesday, a tighter race than the same poll showed several weeks earlier. Trump has taken the lead in online prediction markets such as Predictit and Polymarket.

Investors caution, however, that linking the investment moves to Trump this time is more difficult, as many can also be tied to rising economic optimism following a blowout U.S. jobs report this month and a 50-basis-point interest-rate cut from the Federal Reserve last month.

"Some of this certainly could be being driven by Trump's improved position in the predictive markets," said Steve Sosnick, chief strategist at Interactive Brokers (NASDAQ:IBKR).

Due to strong economic data, however, “it’s really hard to separate cause from effect, much less separate different causes,” he said.

Among the biggest gainers are shares of Trump Media & Technology Group, the former president’s media company, which have broadly tracked Trump’s fortunes in polls and online prediction markets since its listing this year.

Shares are up more than 140% since Sept. 23.

“It’s the trade that is most levered to Trump’s election prospects,” Sosnick said.

Other beneficiaries include private prison operators Geo Group (NYSE:GEO) and CoreCivic (NYSE:CXW), whose shares have risen about 18% and 10%, respectively, this month. Trump has promised to crack down on illegal immigration, which could boost demand for detention centers.

The small cap-focused Russell 2000 is up 4% since Oct. 10 and trades near its highest level since late 2021. Expectations that Trump will keep taxes low and reduce regulation have boosted shares of smaller companies, though analysts believe they are also benefiting from greater confidence in the economy.

In foreign-exchange markets, Trump trades are visible in the dollar’s rebound against a range of currencies, particularly the Mexican peso, strategists said.

The peso, seen as vulnerable to new tariffs Trump plans to impose, is down 4% from its September high. MSCI's gauge for Latin American currencies has slipped over 3% during that period.

"Implied volatility in the dollar-peso pair has been ratcheting up in line with Trump’s gains in betting markets," said Karl Schamotta, chief market strategist at payments company Corpay in Toronto.

Trump said on Sunday he would slap tariffs as high as 200% on vehicles imported from Mexico.

The former president’s economic policies are seen as growth-friendly and a catalyst for inflation, two factors that could translate to higher Treasury yields, which move inversely to bond prices, and a stronger dollar.

The dollar index, which measures the greenback's strength against six major currencies, has risen more than 3% since late September, as investors price in a shallower trajectory for interest-rate cuts. Some of its gains, however, are likely related to greater confidence of a Trump win, wrote Thierry Wizman, global FX & rates strategist at Macquarie.

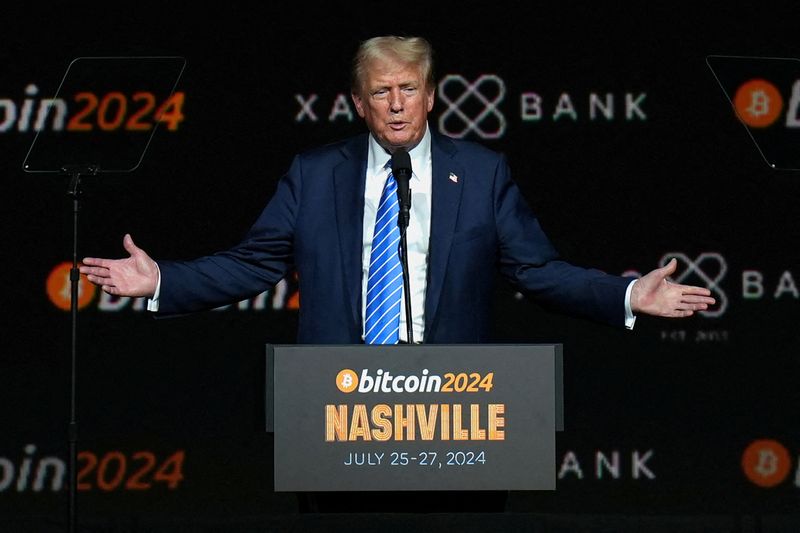

Improved betting-market odds for Trump, who has positioned himself as pro-cryptocurrency, appear to be lifting bitcoin. The world's largest cryptocurrency is up 12% since Oct. 10, a rally that Sean Farrell, head of digital asset strategy at Fundstrat Global Advisors, attributed to rising confidence in a Trump victory.

"If Trump secures a second term, the regulatory-risk-driven discount applied to crypto would likely shrink to near-zero, and investors would need to price in the possibility, however small, of the government adopting a strategic bitcoin reserve," he said.

In government bond markets, some investors believe Trump’s improved standing has spurred a rise in the 10-year term premium - a measure of the compensation investors demand to hold long-term government debt securities - on concerns that the former president’s proposals for lower taxes could increase the budget deficit.

A New York Fed gauge measuring term premium turned positive last week for the first time since July. The move has come amid a broader rise in Treasury yields.

Part of the reason for those moves are expectations of a Trump win, said Matt Eagan, portfolio manager and head of the full discretion team at Loomis, Sayles & Company.

Investing.com-- Most Asian stocks were muted on Friday amid uncertainty over U.S. interest rates and the upcoming presidential election, while Chinese shares turned positive on data showing the economy grew as expected.

Technology stocks clocked relatively smaller losses, while chipmaker TSMC rallied to record highs on stronger-than-expected third-quarter earnings.

Regional markets took muted cues from a mostly flat overnight session on Wall Street. While investors did cheer signs of resilience in the U.S. economy, this enthusiasm was largely undercut by bets on a smaller upcoming interest rate cut by the Federal Reserve.

U.S. stock index futures were flat Asian trade.

Chinese shares rise as GDP meets expectations

China’s Shanghai Shenzhen CSI 300 and Shanghai Composite indexes rose around 1.2% each, recovering sharply from a negative start to the day. Hong Kong’s Hang Seng index rose 1.6% on gains in locally-listed mainland stocks.

Gross domestic data showed China’s economy grew 4.6% year-on-year in the third quarter, as expected. Quarter-on-quarter growth also accelerated, although year-to-date GDP growth still remained below the government’s 5% annual target.

Still, Friday’s gains helped Chinese stocks recoup a bulk of their weekly losses, putting them on track for a muted weekly performance.

Chinese shares had logged heavy losses earlier in the week after Beijing’s signals on more stimulus measures inspired limited confidence, given that the government still left investors wanting for more details on the planned measures.

TSMC hits record high on positive Q3, chipmakers lag

Taiwan’s TSMC (TW:2330) (NYSE:TSM) was an outlier on Friday, with the firm’s Taipei shares surging nearly 6% to a record high.

The world’s biggest contract chipmaker logged stronger-than-expected third-quarter earnings, and also presented an upbeat outlook, as it continued to benefit from robust demand fueled by the artificial intelligence industry.

TSMC is widely considered as a bellwether for the chipmaking industry, and flagged increasing demand from AI for the sector.

But other Asian chipmaking stocks mostly retreated on Friday. The sector was still reeling from weak guidance presented by chip equipment maker ASML (AS:ASML) Holding (NASDAQ:ASML) earlier this week, as the firm said chip demand from applications outside AI was likely to remain weak.

Asian markets muted, head for mild weekly losses

Broader Asian markets kept to a tight range, and were mostly headed for mild weekly declines.

Japan’s Nikkei 225 and TOPIX indexes rose slightly as consumer price index data showed inflation increased slightly more than expected in September, while underlying inflation remained robust.

Australia’s ASX 200 was the worst performer for the day, losing 0.9% as investors locked in profits from a recent record high. South Korea’s KOSPI fell 0.4%.

Futures for India’s Nifty 50 index pointed to a weak open, as the index sank from 25,000 points amid a broad exodus of foreign investors. Some disappointing earnings also weighed.

Investing.com-- Gold prices hit a record high in Asian trade on Friday, benefiting from safe haven demand with just weeks left to a closely contested U.S. presidential election, while an interest rate cut by the European Central Bank also helped.

Spot gold rose 0.4% to a record high of $2,705.26 an ounce, while gold futures expiring in December rose 0.5% to $2,720.15 an ounce.

The yellow metal firmed even as strong U.S. retail sales and labor market data furthered bets that U.S. interest rates will fall at a slower pace in the coming months.

Gold buoyed by pre-election safe haven demand

Bullion prices broke out of a tight trading range seen in the past two weeks, hitting new peaks as the U.S. election approached.

Recent polls showed Vice President Kamala Harris and former president Donald Trump set for a tight presidential race, with less than three weeks left to the ballot.

The disparity in the stances of both candidates spurred increased uncertainty over what the results of the election will entail.

While media polls showed Harris with a small lead over Trump, prediction and betting markets largely leaned towards a Trump victory, sparking more uncertainty over the potential outcome.

Gold was also favored by safe haven demand as the Middle East conflict raged on. Traders were bracing for Israel’s retaliation against Iran over an early-October attack.

Gold brushes off stronger dollar

The yellow metal firmed despite pressure from a stronger dollar, as the greenback hit an over 2-½ month high this week.

The dollar was boosted chiefly by stronger-than-expected retail sales data, and another print showing weekly jobless claims fell, pointing to strength in the labor market.

The readings furthered the notion that the Federal Reserve will cut interest rates by a smaller margin in the coming months.

But a 25 basis point cut by the ECB indicated that major global central banks were still set to cut rates further, with a lower rate environment likely to support gold and other non-yielding assets.

“The precious metal found support from the ECB rate cut, which reminded the market that most central banks have gone into easing mode. This helped it shrug off economic data, which could slow the Fed’s rate cutting cycle,” ANZ analysts wrote in a note, adding that haven demand for gold also remained in play.

Other precious metals were mixed. Platinum futures steadied at $1,005.95 an ounce, while silver futures rose 1% to $32.095 an ounce.

Among industrial metals, copper prices steadied on Friday but were headed for a third week of losses, as recent stimulus measures from top copper importer China largely underwhelmed.

By Andrea Shalal

WASHINGTON (Reuters) - The United States will use restrictive tools like tariffs to push back against China's practice of making far more goods than it needs in order to dominate global markets, White House official Daleep Singh said on Thursday.

Singh, deputy national security adviser for international economics, said the Asian giant has amassed growing market power that it uses for economic and geopolitical leverage, and Washington viewed the costs as unacceptable.

"So that's the problem, and it's not abstract. You can see it in the numbers," Singh told an event hosted by the Alliance for American Manufacturing. "They're a big outlier and we've got to do something about it."

Beijing and Washington have had tense relations for years due to multiple issues ranging from trade tariffs and the origins of COVID-19 to human rights, intellectual property and Taiwan. Singh gave no details on any new measures being considered by Washington.

Data showed that China had a significant overcapacity relative to projected demand for electric vehicles, batteries or semiconductors, Singh said, noting that Chinese producers were reporting "persistent losses."

"We're seeing an unrivaled level and rate of growth in China's subsidies, and ... forget about the numbers, look at their public pronouncements to dominate key sectors and diffuse them with military pre-eminence," Singh said at the event, a week before finance officials from around the world gather in Washington for the annual meetings of the International Monetary Fund and World Bank.

Singh said that "a growing number of countries", including Brazil, India, South Africa and the European Union, were starting to see industrial overcapacity as a major problem like the U.S. did, adding China was using production to gain dominance in a number of sectors.

"China is flooding strategic sectors with supply that's well beyond what global demand can plausibly absorb, and therefore wiping out the competition," he said.

He said China had long used the same tactics for two decades to gain dominance in steel and solar and medical devices, but the trend was now "broadening and intensifying" to include electric vehicles, batteries and semiconductors, where Washington has been investing heavily.

Washington has previously said the U.S. may need to take further and "more creative" actions beyond tariffs to protect U.S. industries and workers against China's growing excess industrial capacity.

U.S. Treasury Secretary Janet Yellen, speaking at a separate Council on Foreign Relations event in New York, said every province in China is competing to try to invest more in advanced manufacturing sectors, such as clean energy and semiconductors.

"So the level of subsidization is utterly enormous. There are many profit-losing firms that are kept in existence. And so there is a gigantic amount of overcapacity that is threatening our own attempts to build in these areas," she said.

ZURICH (Reuters) - Unemployment in Gaza has soared to nearly 80% since the Israel-Hamas war erupted, with the devastated enclave's economy in almost total collapse, the International Labour Organization said on Thursday.

Economic output has shrunk by 85% since the conflict with Israel began a year ago, plunging almost the entire 2.3 million population into poverty, the United Nations agency said.

The conflict has caused "unprecedented and wide-ranging devastation on the labour market and the wider economy across the Occupied Palestinian Territory", the ILO said, referring to Gaza and the West Bank.

In the West Bank, the unemployment rate averaged 34.9% between October 2023 and the end of September 2024, while its economy has contracted by 21.7% compared with the previous 12 months, the ILO said.

Before the crisis, the unemployment rate in Gaza was 45.3% and 14% in the West Bank, according to the Geneva-based organisation.

Gazans either lost their jobs entirely or picked up informal and irregular work "primarily centred on the provision of essential goods and services," the ILO said.

Israel launched its offensive after Hamas-led gunmen attacked on Oct. 7, killing some 1,200 people and taking around 250 hostage, according to Israeli tallies.

Israel's campaign in response has killed more than 42,000 people, according to Gaza's health authorities.

Two-thirds of Gaza's pre-war structures - over 163,000 buildings - have been damaged or flattened, according to U.N. satellite data.

Israel says its operations are aimed at rooting out Hamas militants hiding in tunnels and among Gaza's civilian population.

The crisis has spilled into the West Bank, where Israeli barriers to movement of persons and goods, coupled with broader trade restrictions and supply-chain disruptions, have severely impacted the economy, the ILO said.

Israel says its actions in the West Bank have been necessary to counter Iranian-backed militant groups and to prevent harm to Israeli civilians.

"The impact of the war in the Gaza Strip has taken a toll far beyond loss of life, desperate humanitarian conditions and physical destruction," said ILO regional director for Arab states Ruba Jaradat.

"It has fundamentally altered the socio-economic landscape of Gaza, while also severely impacting the West Bank’s economy and labour market. The impact will be felt for generations to come."

Investing.com-- Gold prices rose slightly in Asian trade on Thursday, remaining close to record highs even as strength in the dollar- on speculation over a second Trump presidency- weighed on broader metal markets.

Among industrial metals, copper prices logged fresh losses as a Chinese government briefing on support for the property market failed to impress.

A drop in Treasury yields helped support gold, as did expectations of interest rates by major central banks. The European Central Bank is widely expected to cut rates by 25 basis points later in the day.

Spot gold rose 0.2% to $2,678.90 an ounce, while gold futures expiring in December rose 0.1% to $2,694.40 an ounce by 00:23 ET (04:23 GMT).

Gold close to record highs amid softer yields, rate cut watch

Spot prices came within spitting distance of a record high of $2,685.96 an ounce on Wednesday.

Bullion prices were supported by weakness in Treasury yields, with the 10-year rate falling 0.5% on Wednesday amid increased speculation that Donald Trump will win a second term.

Trump was seen pulling ahead of Vice President Kamala Harris on online betting markets, while recent media polls showed Harris slightly in front. But with about three weeks left to the ballots, markets are bracing for a tight race.

Trump’s policies are expected to be inflationary- a notion that weighed on Treasury yields and boosted the dollar to its strongest levels since early-August.

Markets were also awaiting more interest rate cuts from major central banks. The European Central Bank is widely expected to cut interest rates at the conclusion of a meeting later on Thursday.

Other precious metal prices were mixed. Platinum futures rose 0.5% to $1,012.40 an ounce, while silver futures fell 0.7% to $31.760 an ounce.

Copper dips as China property cues underwhelm

Benchmark copper futures on the London Metal Exchange fell 0.6% to $9,548.50 a ton, while December copper futures fell 0.6% to $4.3445 a pound.

Both contracts extended recent losses after China’s latest briefing on economic support plans also largely disappointed. China’s housing minister outlined more measures to help support the property market on Thursday- including a bigger whitelist of developers with access to government funding.

But a lack of new features, along with scant details on the implementation of the features, disappointed investors hoping for more bumper measures.

Thursday’s briefing was the latest in a series of stimulus briefings from China, as Beijing mobilizes more support for the economy. But past briefings had also underwhelmed.

This left copper nursing steep losses over the past week, amid doubts over the world’s biggest copper importer. Chinese third-quarter gross domestic product data is due on Friday.

Nevertheless, a quarterly central bank survey suggested the headwinds from the slowing global economy have yet to be fully felt by manufacturers, with the business mood holding up and companies retaining robust spending plans.

That opens up the risk that things could get much bumpier in the coming months, especially as worries over slow global growth join nervousness around the outcome of the U.S. presidential election next month and an escalating conflict in the Middle East.

($1 = 149.5400 yen)

By Makiko Yamazaki

TOKYO (Reuters) - Japan's exports fell for the first time in 10 months in September, data showed on Thursday, a worry for policymakers as any prolonged weakness in global demand will delay plans for a further interest rate hike.

Soft demand in China and slowing U.S. growth have been cited by analysts as a key risk factor for Japan's export-reliant economy and one that could complicate the central bank's path toward fully exiting years of ultra-easy monetary policy.

Total exports dropped 1.7% year-on-year in September, Ministry of Finance data showed, missing a median market forecast for a 0.5% increase and following a revised 5.5% rise in August.

Exports to China, Japan's biggest trading partner, fell 7.3% in September from a year earlier, while those to the United States were down 2.4%, the data showed.

Imports grew 2.1% in September from a year earlier, compared with market forecasts for a 3.2% increase.

As a result, Japan ran a trade deficit of 294.3 billion yen ($1.97 billion) for September, compared with the forecast of a deficit of 237.6 billion yen.

Bank of Japan (BOJ) Governor Kazuo Ueda has highlighted external risks such as U.S. economic uncertainties in his recent dovish commentary, emphasising that policymakers can afford to spend time scrutinising such risks in timing the next interest rate hike.

While the BOJ is expected to keep interest rates steady at its Oct.30-31 meeting, it will roughly maintain its forecast for inflation to stay around its 2% target through March 2027, according to sources familiar with its thinking.

(Reuters) - Goldman Sachs said on Wednesday it expects the U.S. Federal Reserve to deliver consecutive 25-basis-point (bps) interest rate cuts from November 2024 through June 2025 to a terminal rate range of 3.25-3.5%.

Last month, the U.S. central bank cut the overnight rate by half a percentage point, citing greater confidence that inflation will keep receding to its 2% annual target.

The overnight rate, which guides how much interest banks pay each other and affects rates for consumers, is now at 4.75%-5.00%.

Markets are currently pricing in a 94.1% chance for a cut of 25 bps at the Fed's next meeting, with only a 5.9% chance the central bank will hold rates steady, according to CME's Fedwatch Tool.

Goldman Sachs also said it expects the European Central Bank to cut interest rates by 25 bps at its monetary policy meeting on Thursday, and noted it sees sequential 25-bps cuts until the policy rate reaches 2% in June 2025.

By Donny Kwok and James Pomfret

HONG KONG (Reuters) -Hong Kong's leader pledged on Wednesday to reform and revive the economy and financial markets including slashing liquor duties, while seeking to improve dire living conditions for the city's poorest.

John Lee, in his third annual policy address, highlighted the need to "deepen our reforms and explore new growth areas," in line with China's national priorities and recent calls from Beijing for all sectors to unite to promote development and economic growth.

Hong Kong's small and open economy has felt the ripple effects of a slowdown in the Chinese economy and political tensions including a years-long national security crackdown.

It grew by 3.3% in the second quarter from a year earlier, and is forecast to grow 2.5%-3.5% for the year.

Although tourism has rebounded since COVID, with 46 million visitors expected this year, consumption and retail spending remain sluggish, while stock listings have dried up and capital flight remains a challenge.

Lee told Hong Kong's legislature that duties on liquor would be slashed to 10% from 100% for drinks with more than 30% alcohol content, in a bid to stimulate the trade in spirits. The lower duties apply only to spirits priced over HK$200 ($26), and for the portion above that amount.

The move would "promote liquor trade and boost development of high value added industries including logistics and storage, tourism as well as high end food and beverage consumption," Lee said.

He hoped the move would benefit Hong Kong in the way that it became an Asian wine trading hub after wine duties were abolished in 2008.

한국어

한국어

Tiếng Việt

Tiếng Việt

中文

中文