By Devayani Sathyan

BENGALURU (Reuters) - After more than a year of moderate expansion, South Korea's economic growth likely slowed to a near halt last quarter as higher borrowing costs held back domestic demand despite robust exports, a Reuters poll of economists found.

On a quarterly basis, the export-led economy was expected to have expanded a seasonally adjusted 0.1% in the second quarter, according to the median forecast of 21 economists, a sharp slowdown from the 1.3% quarterly growth in January-March.

Seven economists forecast an outright contraction and two expected the economy to flat line. If the median forecast is realised, it would be the slowest growth since late 2022.

On an annual basis, gross domestic product (GDP) likely expanded 2.5%, according to the median forecast from 25 economists polled July 15-22, down from 3.3% in the first quarter.

The data will be published on July 25.

"We expect... GDP data to show growth stalling following a strong expansion in Q1 2024. While high frequency data continued to point to robust exports and manufacturing, these were likely offset by weaknesses in domestic demand," noted Krystal Tan, an economist at ANZ.

Growth in Asia's fourth-largest economy has been largely export-driven since its reopening after the COVID-19 pandemic, while domestic demand has remained subdued as consumers grapple with high borrowing costs.

South Korean households are among the most indebted globally.

"Domestic demand requires support from a less-restrictive monetary policy setting; with inflation converging towards its 2% target, an easing pivot by the Bank of Korea is likely by Q4 2024," Tan added.

The Bank of Korea left its key interest rate unchanged at a 15-year high of 3.50% for the 12th straight meeting in July. However, the central bank said it was time to prepare for a policy pivot.

The latest Reuters poll indicated the first rate cut is likely to come next quarter.

Growth in South Korea is forecast to average 2.5% this year as a faltering economic recovery in China, its largest trading partner, poses a risk alongside domestic concerns.

It was expected to slow to 2.2% next year, a separate Reuters poll showed.

By Howard Schneider

WASHINGTON (Reuters) - U.S. President Joe Biden may not have gotten much credit politically for the thousands of grants and public investments his administration showered across the country, with airport or road projects in places like South Carolina and Wyoming unlikely to dent former President Donald Trump's locked-in status in those deeply conservative states.

It may take years, moreover, to reveal whether what Biden attempted - jump-starting a post-carbon energy transition, reshoring tech production, spreading the wealth to less-prosperous cities, and rebuilding degraded infrastructure - will pay off as his supporters argue in higher productivity, more-secure supply chains, and as a down payment on addressing climate change.

Critics would say the Democratic president ran up the deficit, picked winners in place of private markets, overstepped on issues like student loan forgiveness and anti-trust enforcement, and stoked inflation.

Yet as Biden bowed out of his reelection bid on Sunday, neither supporters nor opponents doubted his ambition to be an economically transformative president by pressing a playbook of progressive economic ideas gestating since the 2007-2009 financial crisis.

Biden didn't wade into the more aggressive and controversial tax ideas some Democrats have pushed to redistribute wealth and income, though that informed ideas like boosting Internal Revenue Service collection efforts.

But he did bring back what used to be called "industrial policy," rebranded it as supply-side economics with a liberal tilt, and tried to tackle problems he felt were either strategic - the need to boost domestic semiconductor production - or moral - underwriting child care and student loans.

Biden's program was "big, dramatic," said Mark Muro, a senior fellow at the Brookings Institution's Metropolitan Policy Program and an advocate of the president's focus on seeding technology investment in areas that have fallen behind economically.

"Biden was able to break through a decade or more of gridlock, 'small ball,' and skepticism about government to go big with a major experiment with investment - in technology, green energy, and infrastructure," Muro said. "Running through it all has been a compelling design focus on places and inclusion" to spread the benefits of innovation beyond traditional hubs like San Francisco and Boston.

'NOT LEGACY-DEFINING'

It was also expensive as well expansive, arguably exacerbating an outbreak of inflation in 2022, was more skeptical of globalization than the vision of Biden's Democratic predecessors, Barack Obama and Bill Clinton, and embraced a broad view of the federal government's role.

Over a consequential first two years, Biden pushed four major pieces of economic legislation through Congress.

One pillar of that program, the $1 trillion infrastructure bill in 2021, was "very reasonable, the type of things you could imagine previous presidents doing," said Michael Strain, a resident scholar and director of economic policy studies at the American Enterprise Institute.

But "that was not legacy-defining. What the president wanted to do was be the next FDR (Franklin Delano Roosevelt), the next Lyndon Johnson," Strain said, referring to the Democratic presidents who introduced the New Deal and Great Society programs that greatly expanded government's economic footprint in the 1930s and 1960s.

At its worst, Strain said he regarded Biden's spending as "reckless," with government debt now equal to 6% of national economic output, the sort of hole usually seen during a recession. Strain also frowned on "silly gimmicks like student debt forgiveness" that have expanded the border of federal help for increasingly middle-class families.

It is hardly the dark travesty painted by Trump, who is seeking to win back the White House after losing the 2020 election to Biden. The unemployment rate under Biden had its longest run below 4% since the 1960s, lasting more than two years. The wage gains enjoyed by U.S. workers have been strongest for lower-paid occupations, and for many have kept pace with inflation.

'MAKING A DIFFERENCE'

In fact Biden and Trump arguably share one important economic trait: The use of deficit spending to keep growth above trend.

Trump relied on a standing Republic playbook of tax cuts that were not offset with spending reductions, while Biden's was something of a new approach for Democrats.

Biden, as Obama's vice president, had a ringside seat for the Democratic president's efforts to counter the 2007-2009 financial crisis with programs now considered too tepid.

The recovery from that deep recession was grindingly slow and scarring. The lesson seemed clear: When a crisis hits, the response should be fast and large.

That was the logic behind Biden's first major economic bill, the $1.9 trillion American Rescue Plan. Enacted less than two months after Biden's Jan. 20, 2021 inauguration, it extended many of the stimulus, unemployment and other payments rolled out by Trump at the outset of the COVID-19 pandemic.

While the recovery effort from the health crisis extended past the end of Trump's term and was largely carried out with bipartisan support, the net result was an unemployment rate that returned to the mid-4% range in about 18 months after the pandemic-triggered recession. By contrast, it took more than seven years to reach that level of joblessness after the financial crisis - a turgid recovery that was particularly tough for blue-collar America and which helped fuel Trump's rise.

Subsequent bills included the bipartisan infrastructure plan, money to boost U.S. semiconductor chip production, and the Inflation Reduction Act, perhaps Biden's most controversial initiative for including incentives for green energy production and electric vehicles in a bill ostensibly to address rising prices.

Some of those programs might well be reversed if Trump wins the Nov. 5 election.

But much of what Biden set in motion is likely to endure, said Mark Zandi, the chief economist at Moody's (NYSE:MCO) Analytics.

The country got through the pandemic with less economic damage than feared, and if the cost of that was inflation, the alternative could have been far more painful in terms of chronic unemployment and lost production, Zandi said. Likewise, the investment in infrastructure and chip production - something seen in the jump in factory investment and the number of road crews spread across U.S. cities - is largely out the door.

It isn't on the scale of what Roosevelt did to address the Great Depression, Zandi said, but it mattered.

"I view it as expansive, large, making a difference, but in the context of traditional macroeconomic policy, not as transformative or changing the playing field," he said. "We are on the same playing field. He just played with bigger players and more muscle."

(Reuters) -There is rarely a dull moment in markets and the week to come will be no exception, with make-or-break U.S. inflation data and tough questions over international financing for Ukraine - all against a backdrop of a fraught U.S. presidential race.

U.S. President Joe Biden's surprise decision on Sunday to pull out of the race for the White House could prompt investors to unwind trades that bet on a Republican victory increasing U.S. fiscal and inflationary pressures.

Earnings will be front and centre, as members of the "Magnificent 7" report their results, along with major banks.

Here's your look at what's happening in markets in the coming week, from Rae Wee in Singapore, Lewis Krauskopf in New York and Naomi Rovnick, Tommy Wilkes and Marc Jones in London.

1/GIVE PCE A CHANCE

U.S. inflation data on July 26 will test growing market expectations that the Fed is all but certain to cut interest rates in the coming months.

June's personal consumption expenditures (PCE) price index is expected to have climbed 0.1% on a monthly basis, according to a Reuters poll.

The release of the PCE report comes after another inflation reading, the consumer price index, fell in June for the first time in four years. That cooler-than-expected report set off a rotation in equities and cemented market expectations that the Fed is primed to cut rates in September.

Several days after CPI, Fed Chair Jerome Powell said second-quarter inflation readings "add somewhat to confidence" that the pace of price increases is returning to the Fed's target in a sustainable fashion.

Investors will also be watching corporate results, as Tesla (NASDAQ:TSLA) and Alphabet (NASDAQ:GOOGL) feature in a busy week for earnings.

2/AD-VANCE WARNING

News that Donald Trump has chosen J.D. Vance as his running mate for November's presidential election has reverberated particularly sharply in emerging markets and nowhere more so than Ukraine.

Trump has long-promised to broker an end to its war with Russia and in Vance he has picked someone who has publicly questioned whether supporting Kyiv is necessarily in the U.S.' interests.

For markets, that is something to watch.

Ukraine has just proposed its first wartime hike in taxes and is intensifying talks on a $20 billion sovereign debt restructuring with the likes of BlackRock (NYSE:BLK) and PIMCO. Eastern European currencies are getting twitchy again.

The U.S. reducing its weapons and support would be a catastrophe for Ukraine. But a swift deal to end hostilities could mean the massive reconstruction effort starts far sooner than many had hoped, even if it would leave plenty of lingering doubts.

3/INFLATION TEST

The Tokyo inflation report on July 26 will be the final check-in on consumer prices before the Bank of Japan (BOJ) meets on July 31, where the prospects of a rate hike from the central bank remain a toss-up.

An acceleration in July's inflation figures could feed expectations for further monetary policy tightening in the near term, though a slowdown would likely see those bets unwind and weigh on the yen.

Analysts say cost pressures from a weak yen, which has fallen some 10% against the dollar this year, could heighten the chance of inflation staying well above the BOJ's 2% target, though that has also inadvertently hurt households.

While Tokyo's latest rounds of suspected intervention have hauled the currency away from a 38-year low, any impact is likely to be short-lived until rate differentials with the U.S. narrow.

4/BANK ON IT

European banks' run of improving profitability and rising share prices faces its latest test, as second-quarter earnings get going in earnest.

Key is net interest income - which banks have seen surge thanks to higher rates - as the European Central Bank looks to cut rates further and the Bank of England prepares to ease. Investors will also want to see how lenders are faring as political uncertainty intensifies - French bank shares fell sharply during recent elections.

A busy Wednesday sees Germany's Deutsche Bank, Britain's Lloyds (LON:LLOY) BNP Paribas (OTC:BNPQY) in France, Spain's Santander (BME:SAN) and Italy's UniCredit all update investors, with more banks reporting the following week.

Analysts say the read-across from U.S. firms that have already reported is that stronger investment banking revenues should boost lenders with large investment bank arms such as Deutsche and Switzerland's UBS, but markets have little tolerance for interest income numbers that disappoint.

5/IN THE (EURO) ZONE

The euro zone economy is proving to be a huge dilemma for the European Central Bank, as overall growth has been sluggish, but strength in the dominant services sector, boosted by tourism, has kept inflation pressures uncomfortably high.

Flash purchasing managers' indices out on July 24 will show if the ECB's challenge is getting any easier.

The euro zone PMIs, based on business managers' observations of price and demand trends, could be especially influential after the ECB held interest rates at 3.75% and resisted offering future guidance, saying it was "data-dependent."

The central bank, which lowered borrowing costs for the first time in five years in June, does see inflation moderating.

Money markets are firmly pricing a September rate cut, supporting euro zone stocks, government bonds and the euro for now, but also raising the threat level of any PMI result that could shift the ECB's view.

(Reuters) - A top U.S. bank regulator's confidential assessments found 11 of the 22 large banks it supervises have "insufficient" or "weak" management of a broad swath of risks ranging from cyberattacks to employee blunders, Bloomberg News reported on Sunday.

About one-third of the banks secured ratings of 3 or below on a 5-point scale for their overall management of risk in confidential assessments by the Office of the Comptroller of the Currency, the report said.

The OCC did not immediately respond to a Reuters request for comment.

The OCC told Bloomberg in a statement that Acting Comptroller Michael Hsu has "consistently discussed the need for banks to guard against complacency and actively manage their risks in order to build and maintain trust in the federal banking system."

The report follows an hours-long global computer systems outage impacting services from airlines to healthcare, shipping and finance, two days ago.

(Fixes typo in paragraph 2)

By Noel Randewich

(Reuters) -A look at the day ahead in Asian markets by Noel Randewich.

Markets face a new U.S. electoral calculus after U.S. President Joe Biden's abrupt announcement Sunday that he will end his campaign against former President Donald Trump for reelection.

Friday's global cyber disruption was a factor in the S&P 500 and Nasdaq posting their worst weeks since April. It was not obvious before exactly what the "Trump trade" was or its overall impact given the focus on Fed policy and other variables. But now investors everywhere will scramble to figure out how to play the sudden uncertainty.

Investors may still be licking their wounds as Asian financial markets gear up after a week that saw worries about Taiwan, global trade and semiconductors rattle tech stocks and ripple across other sectors.

The health of the world's second largest economy is in focus after a key Communist Party meeting last week did little to stoke optimism, and as expectations solidify that Trump will return to the White House.

Pressure for deep changes in how the China's economy functions has risen this year, with consumer and business sentiment near record lows domestically.

China's export dominance has been accentuated by solidifying expectations Trump will win the November U.S. presidential election after the former president formally accepted the Republican Party's nomination.

Asia financial markets open after a dismal week for global stocks that saw MSCI's global index suffer its worst week since April, in large part over worries about trade disruptions, including additional restrictions by Washington on semiconductor sales to China.While Biden endorsed Vice President Kamala Harris to replace him at the top of the Democrat's ticket, it's not yet clear who the party will select. On politics betting website PredictIt, contracts for Harris being the candidate are priced at 83 cents. Contracts for a Trump victory over Harris at the polls are trading at 61 cents, with a potential $1 payout.

Trump has suggested he would impose tariffs of 60% or higher on all Chinese goods, and his choice of populist Ohio Senator J.D. Vance as his running mate provides fresh evidence of what would be a tough U.S. stance on China.

Taiwan must rely on itself for defense given the threat it faces from China, Foreign Minister Lin Chia-lung said on Friday, responding to criticism from Trump that sent global chip stocks skidding on Wednesday.

In Japan, core inflation accelerated for a second straight month in June, data showed on Friday, extending a more than two-year run above the central bank's 2% target. That kept alive market expectations of a near-term interest rate hike, although most economists expect the Bank of Japan (BOJ) to hold off on raising rates at its July 30-31 policy meeting as soft consumption weighs on a fragile economy.

Dollar/yen hardly moved on Friday, wrapping up U.S. trade at 157.50. The BOJ is also wrestling with a weak yen that has crippled households by making food and fuel more expensive. Currency traders will be closely watching the yen after several suspected interventions by the country's central bank to prop it up already this month.

Here are key developments that could provide more direction to Asian markets:

- China's 1-year loan prime rate (July)

- Singapore CPI (June)

- Taiwan export orders (June)

- New Zealand trade balance (June)

SHANGHAI (Reuters) -China surprised markets by lowering a key short-term policy rate and its benchmark lending rates on Monday, in an attempt to boost growth in the world's second-largest economy.

The cuts come after China last week reported weaker-than-expected second-quarter economic data and its top leaders met for a plenum that occurs roughly every five years.

The country is verging on deflation and faces a prolonged property crisis, surging debt and weak consumer and business sentiment. Trade tensions are also flaring, as global leaders grow increasingly wary of China's export dominance.

The People's Bank of China (PBOC) said on Monday it would cut the seven-day reverse repo rate to 1.7% from 1.8%, and would also improve the mechanism of open market operations.

Minutes later, China cut benchmark lending rates by the same margin at the monthly fixing. The one-year loan prime rate (LPR) was lowered to 3.35% from 3.45% previously, while the five-year LPR was reduced to 3.85% from 3.95%.

"PBOC starts to implement pro-growth policy, consistent with the message out of the plenum - authorities are committed to reach whole year GDP target, and policies will adjust after the disappointing Q2 GDP," said Ju Wang, head of Greater China FX & rates strategy at BNP Paribas (OTC:BNPQY).

Wang added that rising expectations for the Federal Reserve to start cutting interest rates also gave the PBOC room to manoeuvre its monetary easing.

China's yuan eased after the rate cuts, and Chinese bond yields fell across the board after the rate cut announcement.

"The fact that PBOC didn't wait for the Fed to cut first indicates that the government recognises the downward pressure on China's economy," said Zhang Zhiwei, president and chief economist at Pinpoint Asset Management.

He expects more rate reduction in China after the Fed enters its rate cut cycle.

China's rate cut is aimed at "strengthening counter-cyclical adjustments to better support the real economy," the PBOC said in a statement.

The announcement also comes after the PBOC said it would revamp its monetary policy transmission channel. PBOC Governor Pan Gongsheng said last month the seven-day reverse repo basically serves the function of the main policy rate.

Investing.com -- It’s set to be a busy week in markets with U.S. inflation data on tap that could help cement expectations for a September rate cut. Earnings season kicks into high gear with the first of the mega caps and a swathe of European banks set to report. Meanwhile PMI data out of the eurozone will bring the path towards the next European Central Bank rate cut more sharply into focus. Here's your look at what's happening in markets for the week ahead.

1. PCE inflation data

U.S. inflation data on Friday will test market expectations that the Federal Reserve is all but certain to cut interest rates in September.

Economists are expecting June's personal consumption expenditures (PCE) price index to have climbed 0.1% for the second straight month, which would bring three-month annualized core inflation down to the slowest pace this year, below the Fed’s 2% target.

The consumer price index fell in June for the first time in four years. That cooler-than-expected report set off a rotation in equities and cemented market expectations that the Fed is primed to cut rates in September.

Several days after CPI, Fed Chair Jerome Powell said second-quarter inflation readings "add somewhat to confidence" that the pace of price increases is returning to the Fed's target in a sustainable fashion.

2. Earnings season gets into full swing

As earnings season enters high gear, bullish investors hope solid corporate results will stem a tumble in technology shares that has cooled this year’s U.S. stock rally.

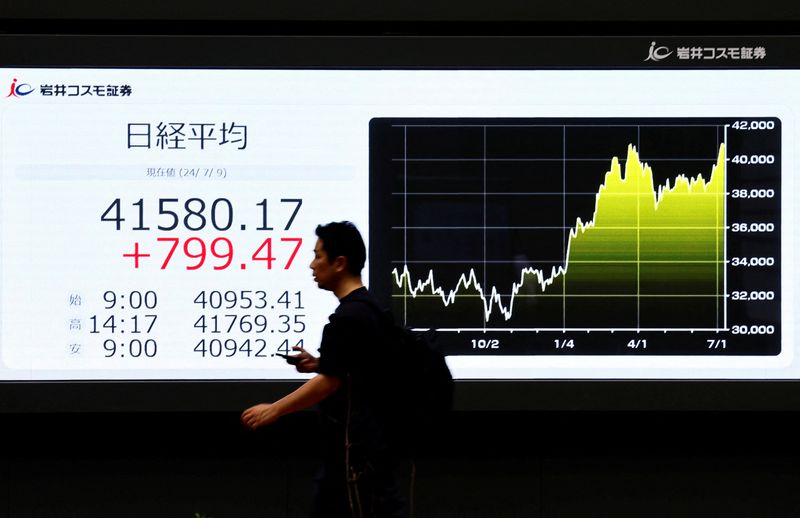

By Rae Wee

SINGAPORE (Reuters) -Asian shares are set to end the week on a sour note, as uncertainty across major economies added to headwinds for investors even as the global rate easing cycle gets under way.

It has been a turbulent week in markets, with a tech sell-off sparked by deepening Sino-U.S. trade tensions, uncertainty over U.S. President Joe Biden's fate in the presidential race, disappointing Chinese economic data and a lacklustre third plenum outcome casting a shadow over the global mood.

In the foreign exchange market, Tokyo's recent bouts of intervention also kept traders on edge.

"We could just be getting a taste of things to come. And that is more turbulence," said Matt Simpson, senior market analyst at City Index.

MSCI's broadest index of Asia-Pacific shares outside Japan slid 1.56% and was headed for its worst week in three months with a nearly 3% loss.

Japan's Nikkei fell to a more than two-week low and was last down 0.09%, extending its sharp 2.4% fall from the previous session.

The Nikkei was on track to lose 2.7% for the week, also its steepest weekly decline in three months.

European shares looked set for a mixed start, with EUROSTOXX 50 futures up 0.08%, while FTSE futures fell 0.4%.

S&P 500 futures tacked on 0.16%, while Nasdaq futures gained 0.3%.

Technology stocks continued to struggle, with South Korea's tech-heavy KOSPI index and Taiwan stocks both falling 1.5% and 2%, respectively.

South Korean chipmaker SK Hynix slid more than 1%, though Japan's Tokyo Electron, a chipmaking equipment manufacturer, rebounded some 2.5%, after an 8.75% tumble on Thursday.

Shares of Taiwan's TSMC, the world's largest contract chipmaker, fell 2.7%, even after the company posted better-than-expected earnings on Thursday and raised its full-year revenue forecast.

In China, investors were left disappointed over the lack of details provided on the implementation steps for achieving economic policy goals at the conclusion of its closely watched plenum on Thursday.

Chinese officials on Friday acknowledged that the sweeping list of economic goals contained "many complex contradictions", pointing to a bumpy road ahead for policy implementation.

Chinese blue-chips were last a touch higher, though the CSI300 Real Estate index slid more than 2%, as an anaemic property sector continued to weigh on China's growth outlook.

The Shanghai Composite Index edged 0.08% lower, while Hong Kong's Hang Seng index fell 2.1%.

"Apart from very broad-brush platitudes devoid of stimulus, economic policy references of quality over quantity may also imply willingness to stomach slower overall growth," said Vishnu Varathan, chief economist for Asia ex-Japan at Mizuho Bank.

The onshore yuan was weaker on the day at 7.2666 per dollar.

RATES VIEW

The euro was last 0.08% lower at $1.0887, having fallen 0.4% in the previous session after the European Central Bank (ECB) kept rates on hold as expected but left the door open to a September cut as it downgraded its view of the euro zone's economic prospects.

"The policy statement gives little away, offering no meaningful changes from June - continuing to stress a data-dependent approach to policy setting," said Nick Rees, FX market analyst at MonFX.

By Leika Kihara

TOKYO (Reuters) -Japan's government cut this year's growth forecast on Friday as consumption took a hit from rising import costs due to a weak yen, highlighting the fragile nature of the economic recovery.

But it projected growth to accelerate next year on robust capital expenditure and consumption, retaining its view the economy will sustain a domestic demand-led recovery.

Some members of the government's top economic council, however, voiced concern over recent weakness in consumption and the pain the yen's fall was inflicting on households.

"We can't overlook the impact a weak yen and rising prices are having on households' purchasing power," the private-sector members of the council told Friday's meeting that discussed the new growth forecasts.

"The government and the Bank of Japan must guide policy with a close eye on recent yen declines," they said.

Prime Minister Fumio Kishida told the meeting that the government must be vigilant about the impact rising prices, driven in part by a weak yen, can have on the economy, according to the Kyodo news agency.

The government releases its economic growth forecasts in January and then revises them around July. They serve as a basis for compiling the state budget.

In the revised estimates, the government cut its economic growth forecast for the current fiscal year ending in March 2025 to 0.9% from 1.3% projected in January.

The new forecast is above private-sector forecasts for 0.4% growth, reflecting government hopes that broadening wage hikes, tax cuts and an extension of fuel subsidies will boost consumer spending.

The government expects the economy to grow 1.2% in fiscal 2025, the estimates showed.

While a weak yen gives exporters a boost, it has become a source of concern for policymakers as it hurts consumption by inflating the cost of fuel and food imports.

The government is suspected to have intervened on several occasions this month to slow down the yen's decline, shifting the market's attention to whether the Bank of Japan would raise interest rates at its two-day policy meeting ending on July 31.

The BOJ is also likely to trim its growth forecast for this fiscal year at the meeting, reflecting a rare unscheduled downgrade to historical gross domestic product (GDP) figures, sources have told Reuters. It currently projects growth of 0.8% in the current fiscal year.

BEIJING (Reuters) - China's Ministry of Commerce said on Friday it will implement anti-dumping duties on propionic acid products originating from the United States for five years from July 21.

The anti-dumping duties are set at 43.5% for all U.S. companies, the ministry said.

한국어

한국어

Tiếng Việt

Tiếng Việt

中文

中文